Photo by Emilie on Unsplash

After my recent edition in which I expressly desired to appeal to a wider audience by, among other things, eschewing the use of acronyms (unsuccessfully), I am now going to offer much more parochial industry commentary on what I think should be the biggest focus for the mortgage origination business in the coming year; specifically, the costs of loan production. So why the picture of a shovel in a ditch above? One, it’s a reminder about an alleged Milton Freidman story about tools, progress, and efficiency, and two, see footnote 15 below.

Apologies in advance for those of you come here for the politics of takes about the importance of process over outcomes, the LSCR emphasis on knowing your compliant RESPA narrative, Yeats’ poetry, 1980’s movie references, Gen X pop culture (a/k/a the Greatest Generation?)[1] and other

evergreen Musings topics.[2] While this edition isn’t going to have much in terms of regulatory guidance or commentary coupled with those themes, I do have a regulatory angle at the end to “reward” my regualtory readers for hearing me out on some business advice first.

Although I’m not normally an “all the business advice you need to know in a minute” type of guy,[3] sometimes there are lessons in a good parable like the “Who Moved My Cheese” book. So, if I can be blunt, to succeed in the mortgage origination business[4] in 2026 and beyond, lenders need to stop pining for another refi wave (or other “manna from Heaven” volume gooser)[5] and figure out how to reduce the cost of production.

Cost of production

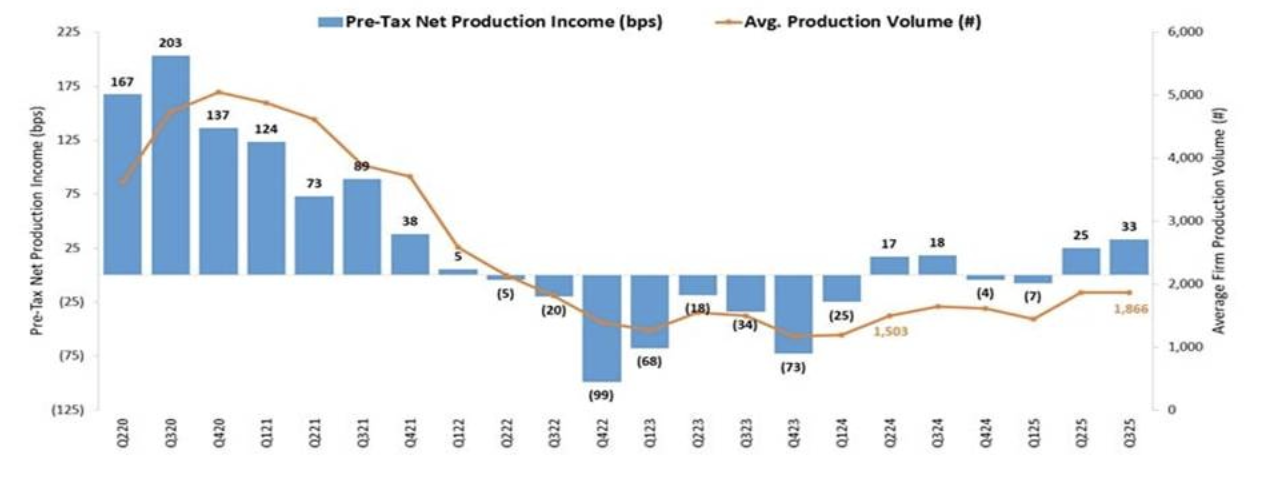

The mortgage industry proved in 2020 and 2021 (and in other refinance boom periods) that it can scale up rapidly and be very profitable when there is massive growth in volume. In my 30 years of experience in this business,[6] however, that never seems to work in the other direction. That is, when volumes decline, the industry is unable to quickly scale downward in its costs.[7] The story for nearly the last 4 years is that breaking even or losing money just to stay in business is the new normal.[8] The graph below from the MBA’s Third Quarter 2025 Quarterly Mortgage Bankers Performance Report shows how this relationship of profits to loan volume looks to people who like charts.[9]

We also learned from MBA[10] that in the 3rd quarter of 2025, total loan production expenses (commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations) increased to 326 basis points, and per-loan costs increased to $11,109 per loan. Freddie Mac put that cost to originate number at $11,800/loan.[11] Of course, when you look at costs per loan it is largely a function of the denominator (volume in terms of number of

loans) because (other than originator commissions) most of the 326 basis points/$11,109 is fixed cost overhead.[12]

Lousy business since 2022

All of this points to the fact that, if my math is correct,[13] since the beginning of 2022, the mortgage business has been a lousy business to be in.[14] Roughly speaking, inflation and home price appreciation (which correlates to loan size) have been about the same over this period, but lenders, as has been the history for this industry, were largely unable to change their production processes to lower their cost structure commensurate with the decline in volume which led to these dismal 4 year results.[15]

There are lots of people talking about cost reduction being critical for the next year. Consultants like Joe Garrett and Mike McAuley have been beating this drum for years, but 4 years of funding losses or basically operating at breakeven should make mortgage company owners reconsider the urgency of the need for dramatic change. Frankly, even commissioned mortgage originators who want their company to remain viable should want to see the cost of production decline (and they might need to consider thier own role in that).

Is AI the answer?

Since there are no raw materials in making a loan,[16] almost all of the cost of production (at least for most distributed retail companies who don’t buy Super Bowl ads or stadium naming rights) is bound up in up in compensating knowledge workers and the systems they use. So, there are two primary levers to reduce costs: lower employment costs[17] and/or lower IT system costs.

As a result, in 2026, mortgage companies need to at least consider if artificial intelligence (AI) can enable scalable cost reductions in staffing and/or systems outlays.[18] Some very smart folks were predicting last year that unless you get on the AI train that you will be left at the station. There are also plenty of AI skeptics, but whether AI is another Dot-com, blockchain/crypto bubble or not, I suspect you’ll see even more smart person predictions about AI use for 2026 (highlighting how data integration is essential AI cost/benefit analysis).

I agree with Rob Chrisman about AI’s potential and the pivotal moment for the mortgage industry we face,

“The real opportunity isn’t chasing shiny “AI for AI’s sake” tools from companies that just learned what a 1003 is. It’s using AI to make the platforms we already depend on smarter and more efficient. But AI alone can’t deliver outcomes. True AI needs to be in the workflow, not adjacent to it. The insights produced often stall without a way to operationalize them. That’s where workflow comes in and independent mortgage bankers are facing a pivotal moment.”

This means companies will need to seamlessly integrate AI into their processes and not just have someone type data from an LOS into an AI system to get an answer only then put that answer back in the LOS. If there isn’t a significant scalable cost savings from using AI, there probably isn’t case to use it.

Change is hard

That said, for a mortgage origination business to successfully pull off meaningful changes, they will likely need to rethink their entire production process from marketing to loan sale and embrace organizational change. This will be challenging for companies who need to retrain or let go employees who often are like family members.[19] In addition to sadness and conflict around layoffs, it is only natural for staff, vendor, and system providers to resist, deny, and thwart changes that might negatively impact them personally. As a result, any real change to the mortgage production process needs to be led and assessed dispassionately from the very top of the organization.

While a refinance (or purchase market) boom doesn’t seem imminent, mortgage bankers will need to be prepared to compete against new entrants with vastly different cost structures and/or processes when that time arrives. If you start now with the hard work of change to implement scalable production tools like AI and perhaps outsourced labor, not only will you be positioned for lower volumes, you will also be able to scale up and profit even more when volumes increase.

Is there a regulatory angle?

Cutting corners on compliance and responsible lending behavior, however, is never advisable for any business with a long-term plan. Even with a “chainsawed” CFPB, virtually all of the same laws and regulations remain in place and many have state law equivalents and private rights of action.

That said, now is a much better time to experiment with new business models as long as there is a good consumer story (narrative) to tell about what you are doing. As noted in my “open letter” to the new CFPB leadership last March, the CFPB acted as a prior restraint and chilling influence on innovation (particularly in use of AI underwriting engines, but also in creating alternative products) out of concern for possible inequitable racial “effects” and by shoehorning of technical and unworkable compliance obligations intended for other products onto innovative products discouraging product innovation.

The recent CFPB proposal to amend ECOA to, among other things, eliminate claims based solely on the effects test/disparate impact, however, demonstrates the totally different federal regulatory environment in which mortgage companies now operate.[20] Moreover, CFPB has signaled that it recognizes the problems with the LO Compensation Rule and most observers are

saying they expect CFPB to provide some relief to enable discounting commissions.[21] This may not make some loan originators happy, but it will be better for consumers, origination costs, and the free market. So, as you consider your process changes, the defanged CFPB should provide more breathing room to innovate (at least for now).

With the holidays rapidly approaching, I’m going to cut this Musing short here (plus you have lots of footnotes too). Good luck in the coming year!

[1] Fooled you on this link-it wasn’t to one of my prior Musings.

[2] Don’t worry. This edition will still have plenty of the beloved footnotes.

[3] I am, however, quite efficient with my time in my legal practice. In fact, I try not to value my legal services based on the time it takes me to complete a project. Rather, to align my interests with that of the client and to enable budgeting, I typically scope out a project and offer a fixed fee for the work.

[4] Setting aside servicing costs and revenues.

[5] Virtually no one is predicting another refinance boom in the near term. Even less likely would be a bailout of sorts from the GSEs or federal government through rate subsidies or expanded credit boxes. Demand side “affordability” initiatives, like FTHB credits (or 50-year amortization mortgages) tend to also increase home prices further eroding affordability. Meanwhile, greater affordability through home price deflation or joblessness causing foreclosure increases don’t seem too appealing. Anyone with better ideas to goose mortgage volumes, please let me know.

[6] While I was just an undergrad economics and political science double major, I was also an in-house bank GC for 15 years, so I think my “Bullring” credentials are sufficient for this lawyer to offer business guidance in his Musings.

[7] Maybe you actually can lose money on every deal (in one year) and make it up in volume (in the next year)?

[8] And, you will lose money on every deal if you don’t make it up in volume. (BTW, the last two footnotes work well for those of you who read the footnotes first).

[9] The rest of you will skip over the chart or may have just stopped reading this Musing entirely after my “if I can be blunt” summary sentence.

[10] Shout out and special thanks to Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. Marina is a person who definitely likes charts and knows mortgage industry costs and revenues like no one else.

[11] I don’t know why, but $11,000+ seems like a ridiculously large number just to originate one home loan.

[12] There’s a whole lot of oxygen being consumed about the rising costs of FICO scores and credit reports right now, but while the industry’s complaints are entirely valid, lowering these “pass-thru” costs will not significantly impact mortgage lender’s profitability.

[13] Dubious assumption. Never trust a lawyer to do math. They say “numbers don’t lie”, so yeah (lawyer joke there).

[14] This is mostly true for mortgage company owners. Commissioned mortgage originators might be doing just fine, but there’s a target on their backs due to the outsized cost they represent and eliminating the LO Comp Rule might change that situation (see infra). So might any efforts to eliminate RESPA’s prohibitions on payments for referrals, but that that is a topic for another day.

[15] Insert your favorite “when you’re in a hole, stop digging” reference here.

[16] Yet, even today, we still haven’t eliminated most of the paper we use to document our work. See Fn. #4 in https://blevy.substack.com/p/ed-93-the-gse-guaranty-credit-boxes

[17] Note that lowering the number of employees has a greater impact than just reduced compensation expense as fewer employees also reduces need for office space and management expense related to employment.

[18] In addition to AI solutions, companies also should consider the outsourcing/nearshoring options available today when designing cost effective production processes. I know a couple good ones run by people who know the mortgage business.

[19] In many mortgage companies, they actually are family members.

[20] Keep in mind that the Fair Housing Act and state law may continue to recognize disparate impact claims.

[21] Although they will most certainly need some staff to propose a rule to amend LO Comp, Acting CFPB Director Vought is planning to shutter the agency in January due to a new funding argument about the lack of Federal Reserve System “combined earnings” that is clearly destined for judicial review (and Musing fodder).